This section is presented

This section was created by the editors. The client has not been given the opportunity to limit or revise the content prior to publication.

by TD Insurance

Links to breadcrumbs

Personal Finance Family Finance

Ron and Mary would have more than enough to achieve their modest goals, says expert

Ron and Mary want to know if they can both retire in six years with a combined annual income of $60,000 after taxes. Photo by Gigi Suhanic/National Post Illustration

Ron and Mary want to know if they can both retire in six years with a combined annual income of $60,000 after taxes. Photo by Gigi Suhanic/National Post Illustration

Reviews and recommendations are unbiased and products are selected independently. Postmedia may earn an affiliate commission for purchases made through links on this page.

Article content

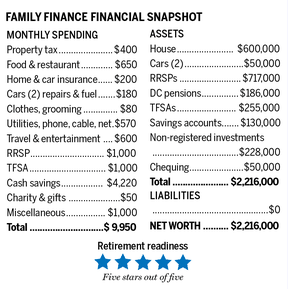

In Alberta, a couple we’ll call Ron and Mary, ages 49 and 45, ponder the end of their respective careers in machinery sales and road management. Ron has worked at his company for 30 years and earns a gross annual income of $90,000. A leader in her niche of the building materials industry, Mary has 17 years with her company and earns $69,000 a year before taxes. They take home $9,950 per month.

Advertisement 2

This ad hasn’t loaded yet, but your article continues below.

Article content

They want to know if they can both retire within six years with a combined annual income of $60,000 after taxes. But they’re also considering a second option, with Ron immediately retiring and Mary working for another decade.

email andrew.allentuck@gmail.com for a free Family Finance analysis

Family Finance asked Eliott Einarson, a financial planner who heads the Winnipeg office of Ottawa-based investment advisory firm Exponent Investment Management Inc., to work with Ron and Mary.

Article content

Calculate their net worth

Ron and Mary both have defined contribution plans that each contribute three percent to the gross pay matched by employers and therefore grow at six percent plus the investment return. Each month they save $1,000 for their RRSPs and $1,000 combined per month for their TFSAs. $4,220 per month goes to unrecorded savings.

Advertisement 3

This ad hasn’t loaded yet, but your article continues below.

Article content

Thus, their assets include their home, appraised at $600,000, for which they paid in full; two DC pensions worth a total of $186,000; $255,000 in their TFSA accounts; RRSPs with a balance of $717,000; $130,000 in a so-called high-yield savings account; and unregistered accounts with a balance of $228,000. Add the $50,000 worth of two cars and $50,000 in their checking accounts and their current net worth is $2,216,000.

Spreading their pensions

If Ron retired this year at age 49 and Mary continued to work until 55, as they considered, they would need $45,000 a year after tax for basic expenses. Mary’s monthly income of $3,800 after taxes would be enough to cover them. But what would happen when Mary retires?

Advertisement 4

This ad hasn’t loaded yet, but your article continues below.

Article content

With no further savings on registered or other accounts, Ron’s $510,000 in registered investments, including his $84,000 defined contribution plan, continued to grow at three percent a year after inflation rose to a value of $685,400 in ten years when Mary turned 55. and would retire.

That amount would make Ron $30,480 a year for the next 36 years at the same rate of growth and distribution of all capital income. The money would run out when Ron is 95 and Mary is 91.

Ron’s unregistered assets and savings held with Mary in name totaling $330,000, a three percent growth after ten years of inflation, would rise to a value of $443,500. That amount would bring in $19,722 annual income for his age of 95. His DC pension and half of this combined unrecorded income, $9,861, would give Ron an income of $40,340 in 2022 dollars.

Advertisement 5

This ad hasn’t loaded yet, but your article continues below.

Article content

Mary’s $393,000 in registered assets, including $102,000 in her DC retirement plan with annual contributions to match, would grow to a value of $577,043 in ten years. That amount would generate an income of $25,660 per year for the next 36 years until her age of 91. If she added half of their combined investment income, $9,861, Mary would have a total income of $35,522 at age 55. Their total annual income would be $75,860. After splits and an average tax of 13 percent, they’d have $66,000 a year or $5,500 a month, right on track.

Synchronize their retirement

Alternatively, they could both continue working for another six years until he is 55 and she is 51, reducing her time to replenish assets but extending his.

In this scenario, his $510,000 would rise to a value of $644,944 in six years. That would make $27,079 a year for 40 years. The unregistered investment and savings account with a combined value of $330,000 growing over six years with $3,000 monthly additions would be worth $633,886. That amount would earn each partner half of $26,625 or $13,313 a year before age 95, giving Ron a total income of $40,392 in 2022 dollars.

Advertisement 6

This ad hasn’t loaded yet, but your article continues below.

Article content

Mary’s registered assets would grow to $496,845 by age 51 with the same assumptions. This capital would generate $20,865 a year until she was 91 years old. Adding her half of the unrecorded income would make $13,312 her gross income of $34,177. Their total income would currently be $74,570 at the start of Ron’s retirement in six years. After splitting the qualifying income and 12 percent average tax, they would have $65,621 or $5,470 per month.

Boosts from TFSAs, CPP and OAS

Their TFSA accounts with a current balance of $255,000 growing without further contributions would be worth $384,432 in six years, assuming contributions remain at $12,000 in total for six years. The accounts can provide a buffer for unexpected expenses or they can withdraw the money for the next 40 years at $16,364 per year for travel or other use.

Advertisement 7

This ad hasn’t loaded yet, but your article continues below.

Article content

In the first case — Ron retires at age 49 — income would rise to $82,364 or $6,865 per month. In the second case, the annual income would be $81,985 per year or $6,830 per month. We’ll average it at $82,174 or $6,850 per month.

By commuting her retirement, this Ottawa official can get her cake and eat it too. But is it worth the risk?

The BC couple has five rental properties, but they don’t own a house – and that is a problem for their pensions

This BC couple in their 40s has $3.1 million in assets, but will it be enough to retire in five years?

Canada Pension Plan and Old Age Security benefits would be available at the age of 65 for each partner. Contribution rates and payouts change, but we estimate that each partner would have 75 percent of potential CPP payments or $10,838 at age 65. At age 65, each partner would have OAS benefits of $7,707 per year per person at 2022 rates. That’s an annual total of $18,545 each or $1,360 per month after 12 percent tax on top of other income when each partner turns 65. Total monthly income would increase to $8,225 when Ron is 65 and $9,585 when Mary is 65.

They would have more than enough to achieve their modest goals.

Retirement stars: five retirement stars ***** out of five

Financial item

email andrew.allentuck@gmail.com for a free Family Finance analysis

Share this article in your social network

Advertisement

This ad hasn’t loaded yet, but your article continues below.

Top Financial Messaging Stories

By clicking the sign up button, you agree to receive the above newsletter from Postmedia Network Inc. receive. You can unsubscribe at any time by clicking the unsubscribe link at the bottom of our emails. Postmedia Network Inc. † 365 Bloor Street East, Toronto, Ontario, M4W 3L4 | 416-383-2300

Thanks for signing up!

Comments

Postmedia is committed to maintaining a lively yet civilized discussion forum and encourages all readers to share their thoughts on our articles. It can take up to an hour for comments to be moderated before appearing on the site. We ask that you keep your comments relevant and respectful. We’ve enabled email notifications – you’ll now receive an email when you get a reply to your comment, there’s an update to a comment thread you’re following, or a user follows comments. Visit our Community Guidelines for more information and details on how to adjust your email settings.

This post Synchronized or staggered? This Alberta couple must decide whether to retire together or be ten years apart

was original published at “https://financialpost.com/personal-finance/family-finance/synchronized-or-staggered-this-alberta-couple-needs-to-decide-whether-to-retire-together-or-a-decade-apart”