This section is presented

This section was created by the editors. The client has not been given the opportunity to limit or revise the content prior to publication.

by TD Insurance

Links to breadcrumbs

Personal Finance Family Finance

Her goal is $60,000 after tax, which in Ontario would require $75,000 in pre-tax income. This plan will help her get there

Publication date:

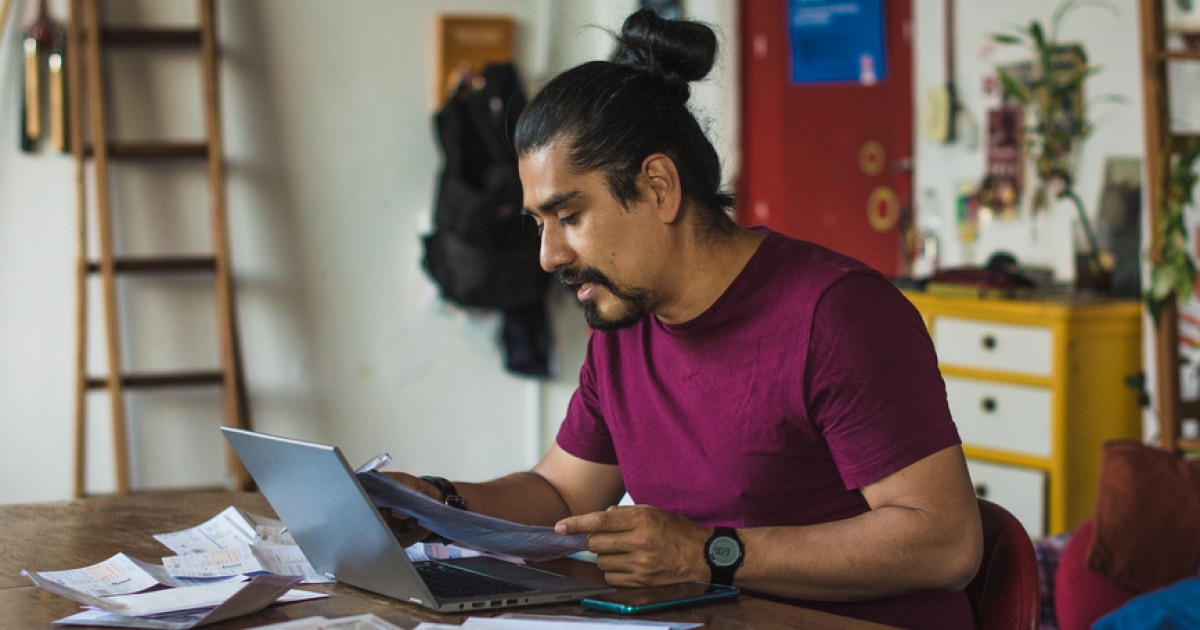

Feb 18 2022 • Feb 18 2022 • Read 5 minutes • Join the conversation  Terri needs to reduce debt by reducing her mortgage and other obligations, as simplification will make long-term planning easier. Photo by Gigi Suhanic/National Post photo illustration

Terri needs to reduce debt by reducing her mortgage and other obligations, as simplification will make long-term planning easier. Photo by Gigi Suhanic/National Post photo illustration

Reviews and recommendations are unbiased and products are selected independently. Postmedia may earn an affiliate commission for purchases made through links on this page.

Article content

A woman we call Terri, 60, lives in Ontario. Her kids are grown and gone, her data management career is thriving. She works for a large corporation and has a pre-tax annual income of $101,520 and a carry-over wage of $67,600 a year. She is a prudent investor and has several stock and real estate assets, including her home and two rental properties. Her problem is figuring out what her assets will pay in retirement income. Her goal is $60,000 after tax, which in Ontario would require $75,000 in pre-tax income. Her problem: can she sustain her income and way of life for three decades? It’s a long-term planning problem, but there is a solution.

Advertisement 2

This ad hasn’t loaded yet, but your article continues below.

Article content

A portfolio of problems

Terri wants to retire, but instead of a date she has set a financial hurdle: She wants to retire when her defined benefit, CPP and later OAS and investment income are enough to pay for the projected expenses of $5,633 per month, including $2,408 in existing debt service and a projected $5,000 per year for travel to see grandchildren and children. She faces questions about when to start CPP, when to sell investment properties, and how to invest $120,000 if and when a child repays a loan she has as an asset in her total net worth.

Article content

Email andrew.allentuck@gmail.com for a free Family Finance analysis.

Family Finance asked Derek Moran, head of Smarter Financial Planning Ltd. in Kelowna, BC, to work with Terri. She should try to reduce her debt by reducing her mortgage and other obligations, Moran suggests, as simplification will make planning easier.

Advertisement 3

This ad hasn’t loaded yet, but your article continues below.

Article content

shrink

Terri would have to sell an $800,000 rental home with a $359,200 mortgage, Moran says. She paid $471,300 for it and lived in it for four or six years of her property, so 4/6ths of the $328,700 profit will be tax-free. The tax formula adds a free year, making it 5/6 tax free. Real estate and legal fees will be $35,000, reducing the capital gain to approximately $293,700. One sixth of the profit is $48,950, half taxable. The tax rate is 43.41 percent on that half, so the tax payable is $10,625. After the dust settles and the mortgage is paid, she has $395,175 left. She can use this money to pay off the $374,000 mortgage on her home, leaving her mortgage free and with $21,000 in cash.

Terri bought the third property, an unfinished flat, for $373,000. She estimates its value at $775,000. It may not be taken into possession until later in 2022. The rent will probably be between one and three percent of the street price. She would like to sell it. If the sale is in 2022 when she’s out of work, her tax rate with no earned income will be lower than if she was sold last year while employed, Moran notes.

Advertisement 4

This ad hasn’t loaded yet, but your article continues below.

Article content

Her profit will be $402,000 less expenses of $35,000, leaving a taxable profit of $367,000. Half of that is taxable, so she would have a taxable profit of $183,500 and a potential tax of $67,530.

She would be left with $367,000 minus $67,530 or $299,470. Take off the $196,000 she owes on a line of credit and she would have $103,470. Add in $21,000 other cash and $126,000 payment for money lent to her son, so she would have $250,470 cash.

Retirement income

Terri’s income is $101,520 per year or $63,660 after tax. If the mansion is sold, she will no longer receive rental income.

Terri’s TFSA, currently $32,000, has $45,500 in dues space. If she added that amount of cash, she would have $77,500 in the TFSA. If that amount grows at three percent per year for 34 years to age 95, it will pay her $3,600 per year from age 61.

Advertisement 5

This ad hasn’t loaded yet, but your article continues below.

Article content

Terri has $416,403 worth of RRSPs. She has $27,506 unused room. If she makes that contribution, the total rises to $443,909. She needs $75,000 pre-tax income and gets $34,000 from her pension. She therefore needs $41,000 per year for eight years, after which the payouts based on the remaining money will drop to $12,324, Moran estimates.

Assuming her income properties are sold and all $929,200 in lines of credit and mortgages are paid off, she will have $171,000 in cash. She needs $30,000 to supplement her pension in 2022.

If the remaining $141,000 grows at three percent per year for 34 years, it will yield about $6,600 per year.

Terri has a defined benefit pension that will pay her $34,000 a year in 2022 and future years. Her CPP should be $10,534 at 65. She can delay the start to 70 with a 42 percent bonus, increasing it to $14,958 per year.

Advertisement 6

This ad hasn’t loaded yet, but your article continues below.

Article content

This BC Couple Should Cut Their $1 Million Rent and Invest in Dividend Stocks to Boost Their Retirement Cash Flow

This Alberta chemist’s guilt is a fleeting part of the mix in retirement

This couple in their thirties with a net worth of $390,000 has decades to save

The specter of inflation adds to the risk of early retirement for this young BC couple

Her OAS will be $7,707 per year using 2022 rates. For age 70, it will be $10,481 per year, including a 36 percent bonus.

If she added her retirement income to 70 in the near future, she would have $34,000 from her job pension, $41,000 from her RRIF, $3,600 from her TFSA, and $6,603 taxable income from the sale of her properties. That works out to $85,203. After 19 percent average tax on all cash flow except TFSA, she would have $69,700 per year or $5,800 per month. That’s more than the $5,000 a month she thinks her living expenses will be in retirement.

By age 70, her RRIF will be reduced to $221,000 and will support an income of $12,324 for 25 years to 95 years. Terri’s total income will then be $34,000 from her retirement, $14,958 from CPP, $3,600 from her TFSA, $10,481 from OAS, and $6,600 from taxable investment income, totaling $81,963. After taxing 20 percent on all cash flow except TFSA, she would have $66,290 per year to spend. That’s $5,525 a month, still enough to reach her goal.

Retirement stars: 3 *** out of 5

Financial item

Email andrew.allentuck@gmail.com for a free Family Finance analysis.

Share this article in your social network

Advertisement

This ad hasn’t loaded yet, but your article continues below.

Top Financial Messaging Stories

By clicking the sign up button, you agree to receive the above newsletter from Postmedia Network Inc. receive. You can unsubscribe at any time by clicking the unsubscribe link at the bottom of our emails. Postmedia Network Inc. † 365 Bloor Street East, Toronto, Ontario, M4W 3L4 | 416-383-2300

Thanks for signing up!

Comments

Postmedia is committed to maintaining a lively yet civilized discussion forum and encourages all readers to share their thoughts on our articles. It can take up to an hour for comments to be moderated before appearing on the site. We ask that you keep your comments relevant and respectful. We’ve enabled email notifications – you’ll now receive an email when you get a reply to your comment, there’s an update to a comment thread you’re following, or a user follows comments. Visit our Community Guidelines for more information and details about customizing your email settings.

This post Ontario woman needs to get rid of real estate and debt to meet her retirement income goal

was original published at “https://financialpost.com/personal-finance/family-finance/this-ontario-women-should-shed-real-estate-and-debt-to-meet-her-retirement-income-goal”