This section is presented

This section was created by the editors. The client has not been given the opportunity to limit or revise the content prior to publication.

by TD Insurance

Links to breadcrumbs

Personal Finance Family Finance

Expert says they should sell some rental properties and buy a home of their own

Squeezing retirement income from rental properties is more difficult than just retirement calculations.

Squeezing retirement income from rental properties is more difficult than just retirement calculations.

Reviews and recommendations are unbiased and products are selected independently. Postmedia may earn an affiliate commission for purchases made through links on this page.

Article content

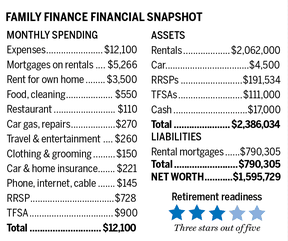

A couple we’ll call Ralph, 64, and Lucy, 60, live in British Columbia. Ralph is an academic specializing in English literature, and Lucy is a sculptor. Together they have five rental properties, all of which are profitable, but they do not own a home, an ironic state of affairs with significant tax implications. Their monthly after-tax income is $12,100. Their goal is to retire in five years with $7,000 in after-tax retirement income.

Advertisement 2

This ad hasn’t loaded yet, but your article continues below.

Article content

Email andrew.allentuck@gmail.com for a Free Family Finance Analysis

Family Finance asked Derek Moran, head of Smarter Financial Planning Ltd. in Kelowna, BC, to work with the couple.

About that real estate…

The first order of business is their real estate ownership, Moran says. Their status as homeless landlords means they have to pay $3,500 in rent each month for their own digs. Still, they don’t have the tax advantage of being able to sell a primary residence — if they had one — without taxing profits.

Article content

In addition, as tenants, they must cover landlord costs — including property taxes — that are part of the costs tenants ultimately pay. But they could defer paying property taxes on their own home in BC at a cost of one percent per year, though it may increase a little, with refunds when their own home is sold. There is no comparable property tax deferral for landlords or tenants. Meanwhile, the rents they collect are taxable after expenses.

Advertisement 3

This ad hasn’t loaded yet, but your article continues below.

Article content

“They have to sell some rental properties and buy their own house,” Moran says.

The core problem is property rationalization, because when you add in withheld income after deductions, mortgage payments, and all taxes, there is only $263 a month of income from $2,062,000 in rentals. “It’s a very tax-inefficient situation,” he adds.

The savings equations

Next, the couple needs to tackle retirement savings. In their tax brackets, RRSPs are more beneficial than TFSAs.

Lucy currently has $144,534 in her RRSP and $90,000 in dues. Ralph has $47,000 in his RRSP and another $47,000 in space, and should immediately consider transferring money from his TFSA to give them additional tax credits.

If he does, their current total of $238,534, growing at three percent post-inflation per year, will become $276,532 in five years and support an indexed, divisible, and taxable RRSP income of $13,698 per year until Lucy’s 95 years of age. .

Advertisement 4

This ad hasn’t loaded yet, but your article continues below.

Article content

Apart from the transfer, Ralph is not allowed to add anything to his RRSPs. The federal pension adjustment, which limits RRSP space for individuals who already contribute 18 percent of income, will block further RRSP contributions.

So the TFSAs, which currently have a balance of $111,000, will have a balance of $64,000 after the transfer.

They paid off an additional $39,000 a year on the rental mortgages. If they instead put that in the TFSAs for five years and grow it at three percent above inflation, it should become $287,461 by 2022 dollars, Moran calculates. That capital would support untaxed payouts of $14,238 for the age of 30 to Lucy’s age 95.

Increase future income

Squeezing retirement income out of rents is harder than just retirement calculations. The properties generate $64,613 a year in net rent, but much of this has to go toward principal repayment, which is not tax-deductible. Choosing which of the five is difficult. The criterion to be used should be the minimization of capital gains. Two units have valued relatively little about their costs. A sale would free up about $800,000 in cash that they could use to buy a home.

Advertisement 5

This ad hasn’t loaded yet, but your article continues below.

Article content

With two sold, net rent would drop to $23,506 per year. We will use this figure. The total cost of home ownership would likely be less than the $42,000 a year the couple currently pays in rent. Over the next five years, that would be a savings of $210,000 in rent paid with after-tax dollars. They’d waive $22,000 a year or $100,000 total for five years for taxable income units sold, Moran estimates, so they’d be $100,000 ahead in five years.

Ralph is eligible for the full annual OAS of $7,707 plus a deferral bonus of 7.2 percent per year — if he starts at age 69, that would be $9,926 per year. Lucy will have OAS benefits at age 65 based on a 38-year residency in Canada of the 40 required for full benefits, net $7,322 per year. That’s a total of $17,284 per year.

Advertisement 6

This ad hasn’t loaded yet, but your article continues below.

Article content

Upon retirement from when Ralph is 69 and Lucy 65, their base cash flow will be Ralph’s $1,200 monthly or $14,400 annual defined benefit pension. He will have a CPP retirement income of $19,300 per year based on an 8.4 percent benefit increase per year for four years of work after age 65. Lucy will have $7,332 CPP income. They can add $13,698 RRSP income, $14,238 TFSA cash flow, $17,284 combined OAS, and $23,506 rental income for a total retirement income of $109,623 before splits.

Summary pension income

Splitting qualifying taxable income (excluding TFSA income) and an average of 13 percent, they would have about $97,000 per year to spend or $8,100 per month.

With rent they currently pay, $3,500 per month, removed, their current monthly allotment, $12,100, would drop to $8,600. Also, $1,628 would no longer go toward RRSP and TFSA savings. They would save a total of $5,128 per month.

Advertisement 7

This ad hasn’t loaded yet, but your article continues below.

Article content

This BC couple in their 40s has $3.1 million in assets, but will it be enough to retire in five years?

This Ontario woman may have to downsize, work part-time to meet her retirement goals

A kitchen reno put a dent in this Alberta teacher’s TFSA. Now she has to catch up for her retirement

Some of their savings could be spent on financing their new home following a cash-based down payment harvested from the sale of the two rental units.

They wouldn’t pay rent for their homes, sell their own homes without capital gains tax, and even defer the payment of property taxes through a BC program that allows seniors to defer such taxes by one percent instead of raising interest, but perhaps a little more as interest rates rise with taxes deferred to be paid when their home is sold.

Rationalizing home ownership and transferring the rent they pay for their home in mortgage payments, delaying retirement until Ralph’s 69 and Lucy’s age 65, and applying the BC property tax deferral credit will allow the couple to exceed their monthly $7,000. after-tax target for retirement income, concludes Moran. “This is a case where less is more. Simplicity is clearly its own reward.”

Retirement stars: three out of five

Financial item

Email andrew.allentuck@gmail.com for a Free Family Finance Analysis

Share this article in your social network

Advertisement

This ad hasn’t loaded yet, but your article continues below.

Top Financial Messaging Stories

By clicking the sign up button, you agree to receive the above newsletter from Postmedia Network Inc. receive. You can unsubscribe at any time by clicking the unsubscribe link at the bottom of our emails. Postmedia Network Inc. † 365 Bloor Street East, Toronto, Ontario, M4W 3L4 | 416-383-2300

Thanks for signing up!

Comments

Postmedia is committed to maintaining a lively yet civilized discussion forum and encourages all readers to share their thoughts on our articles. It can take up to an hour for comments to be moderated before appearing on the site. We ask that you keep your comments relevant and respectful. We’ve enabled email notifications – you’ll now receive an email when you get a reply to your comment, there’s an update to a comment thread you’re following, or a user follows comments. Visit our Community Guidelines for more information and details on how to adjust your email settings.

This post The BC couple has five rental properties, but they don’t own a house – and that is a problem for their pensions

was original published at “https://financialpost.com/personal-finance/family-finance/b-c-couple-has-five-rentals-but-doesnt-own-their-own-home-and-thats-a-problem-for-retirement”