This section is presented

This section was created by the editors. The client has not been given the opportunity to limit or revise the content prior to publication.

by TD Insurance

Links to breadcrumbs

Personal Finance Family Finance

This dish is expensive: Annuities sold by profit-seeking insurance companies aren’t cheap, expert says

Publication date:

25 Mar 2022 • 6 hours ago • 5 minutes read • 7 Replies  Lucille wants to retire next year, at the age of 49, and is considering taking the surrender value of her pension. Photo by Gigi Suhanic/National Post Illustration

Lucille wants to retire next year, at the age of 49, and is considering taking the surrender value of her pension. Photo by Gigi Suhanic/National Post Illustration

Reviews and recommendations are unbiased and products are selected independently. Postmedia may earn an affiliate commission for purchases made through links on this page.

Article content

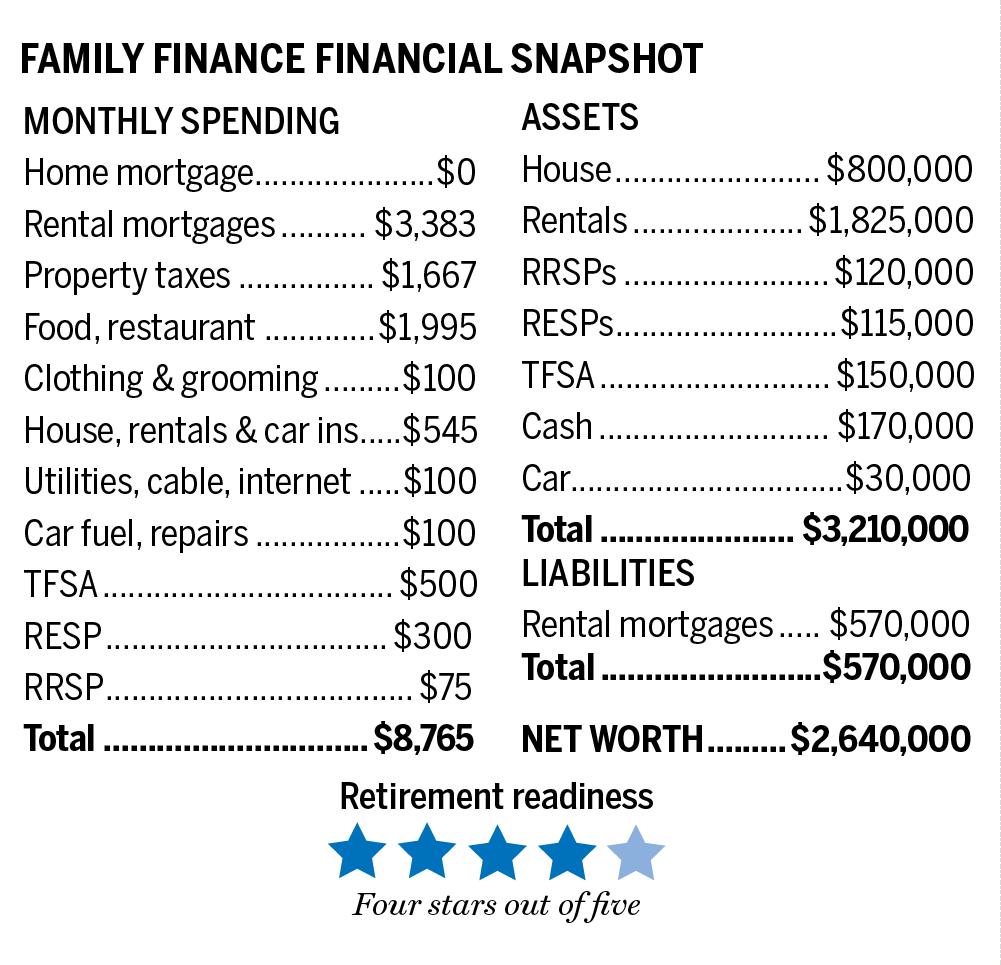

In Ottawa, a woman we’ll call Lucille, 48, works for the federal government. She has three children, all in their teens with adequate RESPs, an $800,000 home, three rental properties with an estimated total value of $1,825,000, and $570,000 in debt before the rent.

Advertisement 2

This ad hasn’t loaded yet, but your article continues below.

Article content

Lucille wants to retire next year, at the age of 49, and is considering taking the surrender value of her pension. That’s the amount of money it takes to generate expected retirement income, which would be $48,000 a year at age 55, the earliest year she can receive income. With interest rates still low, it takes a lot of money to generate a promised retirement income. So it is a good time to think about whether or not to pay out and take the surrendered value. Lucille earns $116,000 a year and has $49,217 in net rental income. After her average tax rate, 36.39 percent, which equates to $60,043 tax, she has an income of $105,174 per year or $8,765 per month.

Article content

email andrew.allentuck@gmail.com for a free Family Finance analysis

The commuted value of Lucille’s federal pension is $852,000 for two decades of work. She would invest it for what she believes would be a higher return than the usual high single digit returns that federal pensions generate. The rules of the process are that she must accept $342,000 in a retirement account, a LIRA, and leave with about $510,000 in taxable money. The tax would cost about half that amount, leaving her about $255,000 for her own investments.

Advertisement 3

This ad hasn’t loaded yet, but your article continues below.

Article content

Family Finance asked Derek Moran, head of Smarter Financial Planning Ltd. in Kelowna, BC, to work with Lucille.

Compare pensions

Lucille has achieved low double-digit returns on her savings and is an impressive investor. Beating a fully indexed federal pension isn’t all about returns, though. A defined benefit plan is ageless. The beneficiary cannot survive. It is bulletproof in the sense that it is much more diversified than what an individual can achieve and is guaranteed not to lose value to any level of inflation. The downside is that the capital in a possible DB pension does not belong to the beneficiary. In this case, it belongs to the government of Canada.

The difference between leaving the DB pension and taking the money is whether she needs the potentially higher return she could earn on the surrendered value, with the understanding that the return could also be lower. The essence of the difference between a government DB pension and a private investment is security. No stock market flop can write off Canada’s government pension plan.

Advertisement 4

This ad hasn’t loaded yet, but your article continues below.

Article content

Plus, payouts are indexed, so if inflation rises, retirees are protected. However, if Lucille takes the converted value, the money is hers to use as collateral for loans or to transfer by will to family or charities. In addition, her own surrender money can be used to purchase a life insurance annuity that can last until her death, even if she lives to be 100 years old or more. This is one way to get her cake – control at least some of her possessions – and eat it. But this dish is expensive: Annuities sold by for-profit insurance companies are not cheap.

Matching returns

Taking the surrendered value turns out to be partly a life or death decision. By age 90, she should earn an average annual return of eight percent post-inflation but pre-tax to beat DB’s retirement, Moran estimates. Giving up her federal DB pension could reduce other benefits, such as dental and medical supplies available in the Canadian Pensions Public Service.

Advertisement 5

This ad hasn’t loaded yet, but your article continues below.

Article content

Lucille has a net worth of $2.64 million excluding her retirement. After deducting the mortgage repayment of the rent, its book value is less than one percent. Its largest investment commitment concerns three rentals, all efficient investments. The property’s value of $1,825,000 of rent minus the $570,000 of mortgage debt leaves $1,255,000. After taxes, flat costs, interest only on the mortgages, maintenance and accounting, she has a net rent of $49,217. The rent is taxed as ordinary income at a marginal rate of 50.23 percent in her bracket, but she could only pay 35.87 percent in her tax bracket on Canadian stock after the dividend tax credit is applied. That makes inventory more tax efficient and far fewer problems with maintenance, breakage or rent failure by tenants, Moran notes.

Advertisement 6

This ad hasn’t loaded yet, but your article continues below.

Article content

Estimating Retirement Income

Before the age of 55 and the start of her DB retirement, Lucille’s RRSP would yield $4,976 per year. Her TFSA would add $6,220 per year, taxable investment income $19,050 per year and net rent $49,217 per year. That’s a total of $79,463. After 20 percent average tax, she would have an income of $5,297 per month. That’s less than current costs minus savings. Some part-time work would be required.

From 55 to 65, she was able to add her $48,000 pension to increase the income to $127,463. After 25 percent average tax, her income would be $95,597 per year or $7,970 per month. That would cover current costs without savings

The BC couple has five rental properties, but they don’t own a house – and that is a problem for their pensions

This BC couple in their 40s has $3.1 million in assets, but will it be enough to retire in five years?

This Ontario woman may have to downsize, work part-time to meet her retirement goals

Advertisement 7

This ad hasn’t loaded yet, but your article continues below.

Article content

From age 65, she was able to add $9,389 estimated Canada Pension Plan and $7,707 OAS income for a total income of $144,560. She would pay 25 percent average tax. The chargeback that starts at $79,054 and tax revenue of 15 percent on that amount would take back all of her OAS. Her final income at 65 would be $108,420 a year or $9,035 a month, more than enough to cover her expenses.

The effect of choosing to take the surrendered value of her pension is to add uncertainty. The upper limit on her savings, including surrendered value, could be a return of 10 percent per annum before tax. Or more. The lower limit could be the total loss of her commuted pension.

Lucille can choose security and no control over much of her retirement savings or commute, pay hefty taxes, and try to beat the federally indexed defined benefit return. You could, but there are shocks to the best plans. In a market collapse, she may need strong nerves. If she keeps the DB pension, she can yawn and get back to what she likes to do.

4 pension stars **** out of 5

Financial item

email andrew.allentuck@gmail.com for a free Family Finance analysis

Share this article in your social network

Advertisement

This ad hasn’t loaded yet, but your article continues below.

Top Financial Messaging Stories

By clicking the sign up button, you agree to receive the above newsletter from Postmedia Network Inc. receive. You can unsubscribe at any time by clicking the unsubscribe link at the bottom of our emails. Postmedia Network Inc. † 365 Bloor Street East, Toronto, Ontario, M4W 3L4 | 416-383-2300

Thanks for signing up!

Comments

Postmedia is committed to maintaining a lively yet civilized discussion forum and encourages all readers to share their thoughts on our articles. It can take up to an hour for comments to be moderated before appearing on the site. We ask that you keep your comments relevant and respectful. We’ve enabled email notifications – you’ll now receive an email when you get a reply to your comment, there’s an update to a comment thread you’re following, or a user follows comments. Visit our Community Guidelines for more information and details about customizing your email settings.

This post By commuting her retirement, this Ottawa official can get her cake and eat it too. But is it worth the risk?

was original published at “https://financialpost.com/personal-finance/family-finance/commuting-her-pension-could-let-this-ottawa-civil-servant-have-her-cake-and-eat-it-too-but-is-it-worth-the-risk”